New York Times best-selling author Pamela Yellen outlines the simple strategy to get rid of financial stress.

Imagine this: A somber-looking man with the wire rim spectacles faces you across his imposing desk. “I’m sorry, but you have a serious condition that we must address.” You take a deep breath and steel yourself. He sighs deeply. “I’m so sorry to tell you this, but your financial pyramid is upside down.” You gasp and clutch your chest while the music from “Jaws” begins to play in the background… Da Dum Da Dum…

Have I lost you completely?

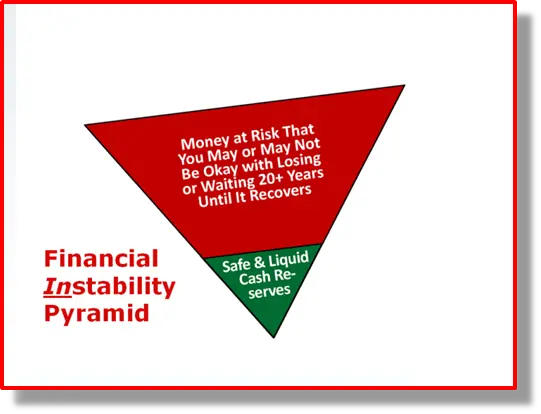

You may not even know that your finances form a pyramid shape. But if you’re like most people, they do. Yours probably looks something like this:

In an upside-down pyramid, the vast majority of financial assets are in the “money at risk” sector – subject to the volatility of the stock market, the real estate market, and other markets. With most of your eggs in that risk-prone basket, you can be flush today and destitute tomorrow. It’s totally out of your control.

In an upside-down pyramid, the only money that’s easy to get your hands on and that’s certain to be there when you need it is in the small “cash reserves” sector, that tiny section your whole pyramid teeters on. It’s like wearing 5½-inch stilettos while navigating a rope bridge swaying in a high wind over the Grand Canyon! And that, my friend, is why you hear the da-dum da-dum from “Jaws” in the background.

Too many people live paycheck to paycheck and don’t sock away anything on a regular basis. Of those who do put something away, most tend to invest (which goes into the larger “money at risk” sector) rather than save (the cash reserves sector). After the bills are paid, they contribute any “extra” money to their 401(k)s, IRAs. Other folks use extra money to pay off their mortgages faster. The result?

More than half – 56% – of Americans say they would be unable to cover an unexpected $1,000 bill with savings, according to a recent survey by Bankrate. Instead of drawing on their emergency savings funds, many people would have to go into debt, borrowing money from family and friends, taking a personal loan from a bank or charging a credit card.

Over the last five years, how many times have you run into an expense you hadn’t anticipated? Maybe your adult child needed help or you got hit with a tax bill you didn’t see coming. Maybe a favorite pet had a health emergency or you found a job opportunity that meant relocating across the country. Big and little financial “surprises” are a given in life.

And it’s not just about the unexpected expenses. With inflation hitting 40-year highs, close to two-thirds of Americans are living paycheck to paycheck. This has become the “dominant lifestyle across income brackets,” according to Anuj Nayar, financial health officer for LendingClub.

Ever been in financial stress … or close?

What about losing your source of income altogether? We all know people who lost their jobs during the pandemic. Maybe you were one of them. Following the Great Recession, CNN Money reported that almost 5½ million Americans had been out of work for more than six months. That was about half of the nation’s unemployed.

So when financial gurus claim you only need three to six months of income in your rainy day fund to be safe and secure, they’re doing you a disservice that could lead to financial stress.

How Much Money Do You Really Need to Have in Your Rainy Day Fund?

Without a substantial rainy day fund of safe and liquid cash reserves of at least two years’ worth of income, you’re putting your financial future at risk. If you lose your job or incur a huge unexpected medical expense and you don’t have large cash reserves, what are your options?

Put it on your credit cards?

Even if your credit lines can handle it (could your credit cards cover being out of work for eight months or a major health challenge?), you could find yourself in a cycle of debt and financial stress that is nearly impossible to dig out of. Putting emergency needs on credit cards can lower your credit rating (increased debt to income ratio), which can lessen your ability to borrow at reasonable rates and may even cause your existing credit card rates to rise. And credit card debts can be extremely expensive in the long run if you can’t pay them off quickly.

Take out a personal loan?

As Mark Twain once said, “A banker is a fellow who lends you his umbrella when the sun is shining but wants it back the minute it begins to rain.” Bankers are thrilled to lend you money when you don’t particularly need it. But when things get tight and you’re in trouble and feeling financial stress, your banker is not so magnanimous.

Who does want your business in those times? Subprime lenders, payday loan shops, and predatory lenders. All of them will charge you extremely high interest rates, and, while these guys no longer collect using baseball bats, if you get behind, your credit rating can get dinged with more black marks than a well-used target at the pistol range.

Sell your investments?

If your investments are sitting at the top of the market, good for you! Unfortunately, that usually isn’t the case when you really need to cash out of your investments. Whether it’s art or real estate or stocks, if you have to sell quickly when you suffer financial stress, you’ll usually take a hit. And if that investment is something you were counting on to fund your retirement, you’ve just robbed yourself and your future security.

Withdraw from your retirement accounts?

This can be a very expensive prospect and can actually increase financial stress. If you withdraw money from most conventional retirement accounts before you’re 59½, you’ll not only pay taxes on the money but you’ll also pay a 10% penalty. Readers can get a free copy of my latest book, “Rescue Your Retirement: Five Wealth-Killing Traps of 401(k)s, IRAs and Roth Plans – and How to Avoid Them,” by going to www.SendTheFreeBook.com.

Borrow from friends or family?

As one author put it, “Borrowing money from people you know can be a great idea or it can be fraught with more danger than playing hopscotch in a minefield.”

Whether it’s your parents, your wealthy golf buddy, or your kids (!), your relationship will too often take a negative turn, adding extra stress on top of the stress of your financial need.

3 Key financial stress questions to ask yourself…

- Will having only three to six months of cash reserves (the amount the gurus typically recommend) really give you peace of mind and let you sleep at night?

- Will just three to six months of cash reserves help you get where you want to go without taking unnecessary risk?

- Will just three to six months of cash reserves allow you to be in charge of your money? Will you – not your employer or the economy or circumstances – have control?

Probably not. It’s a right-side-up pyramid that forms the foundation of a financially stress-free life:

At the top, you have speculative investments like stocks, real estate, commodities, or collectibles. Even if the shenanigans of some greedy investment bank cause the stock market to implode and blow the top off this pyramid, your pyramid won’t come crashing down. You’d be pretty ticked, but you and your family would still be okay.

The second tier includes safer assets such as municipal bonds, investment-grade corporate bonds, and money market funds. And the bottom tier contains assets that are liquid and completely safe, such as savings accounts, whole life insurance policies, short-term CDs and money market accounts.

Imagine how it would feel if your own financial pyramid looked like that right-side-up pyramid!

Cash reserves are the foundation of your pyramid

It’s the difference between sipping piña coladas on a balmy beach and running with the bulls at Pamplona with a bright red bull’s eye painted on your back. A foundation built on savings gives you stability, accessible resources, and restful nights. A foundation built on the inherent risk of investments? Pull out the Dramamine and Ambien!

This brings us to “savings” versus “investments.” Is there a difference between saving money and investing money? Absolutely! To save means to place money in a vehicle that is safe and has guaranteed growth. A savings vehicle is the best place for money you can’t afford to lose. You are certain your money will be there when you need it.

In contrast, to invest means to place money in a financial vehicle or an asset that has a certain amount of risk. You hope to make a gain, but it’s not guaranteed. In fact, you might even lose all the money you originally invested. The only money you should invest is money you can afford to lose – or money that you can let languish in the market for at least 20 years, if necessary until it recovers its value after a market downturn. Note: 20 years isn’t just some arbitrary number I plucked from air. Since 1929, we’ve had three crashes that took nearly two decades – or longer – to recover from.

Savings are safe. Investments are risky. It’s that simple. If someone tries to tell you an investment is risk-free, ask them to put it in writing that you are guaranteed to get all your money back and exactly who is making that guarantee. Then have them sign and date the paper. Keep it in a safe place. You’ll need it when you go to court. A better idea: For true financial peace of mind and fixing financial stress, build a financial pyramid that is right-side up!

Pamela Yellen is founder of Bank On Yourself, a financial investigator and the author of two New York Times best-selling books.